Intergenerational equity - one indicator looking ok

Data alert | ABS Lending Commitments released

A frequently overlooked yet revealing economic indicator is the proportion of new home loan commitments going to first home buyers. It is a deceptively simple statistic, yet it provides important insight into intergenerational equity, market accessibility for younger Australians.

Each quarter, the Australian Bureau of Statistics releases a data series titled Loan Commitments, which reports the number and value of new mortgages issued by authorised deposit-taking institutions (banks). Within that release it is possible to derive a the metric of the percentage of housing loans going to first home buyers.

This figure captures the share of new housing finance flowing to those attempting to enter the property market for the first time—typically younger households. It is a telling measure of whether rising prices, interest rate shifts, or regulatory settings are tilting the housing ladder toward or against new entrants.

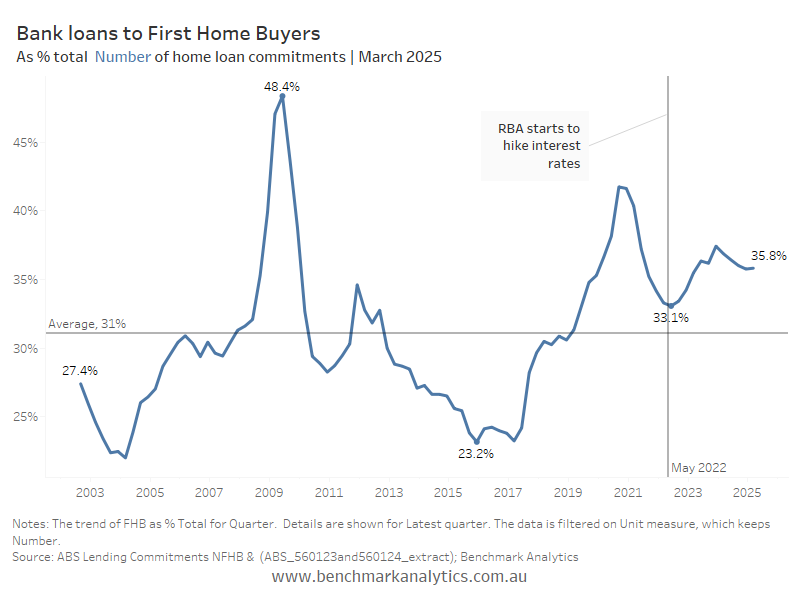

Since the series began in 2002, the average proportion of loans going to first home buyers has been approximately 31%. However, recent data shows a somewhat unexpected trend.

When the Reserve Bank of Australia began raising the cash rate in May 2022 to combat inflation, many assumed that rising interest rates would disproportionally impact households more dependent on bank finance, and benefit those with existing houses.

When the RBA began hiking rates in May of 2022, the share of first home buyers getting finance was 33.1%. After rates started going up, this share increased to to a high of 37% in December 2023.

The relative resilience of first home buyers is politically and economically significant.

Whatever the cause, the result is clear: on this specific metric, intergenerational access to housing finance has held firm—and even improved—during a period of monetary tightening.

Of course, this does not mean that the housing market is fair or efficient in all respects. Dwelling prices remain high by international standards; land use restrictions and supply constraints continue to push up costs. But in the fog of housing policy debate, this statistic offers a shaft of clarity: first home buyers are maintaining their foothold.

See chart: